IRS released Notice 2020-18.

https://www.irs.gov/pub/irs-drop/n-20-18.pdf

Please make sure you check your state specific deadlines. Some have moved their deadlines, but some have not.

IRS released Notice 2020-18.

https://www.irs.gov/pub/irs-drop/n-20-18.pdf

Please make sure you check your state specific deadlines. Some have moved their deadlines, but some have not.

The IRS has identified a new version of a phishing email scam targeting tax professionals. The fake email states the preparer’s EFIN has been put on a temporarily hold and warns the EFIN will be suspended unless the preparers open an embedded document and confirm or deny that they submitted the Form 1040. The embedded “1040” document likely contains malware.

The IRS reminds all tax professionals that they are targets of cybercriminals seeking to steal client data or the practitioners’ identities. Thieves use many variations of phishing emails such as this. The fake emails are characterized by an urgent message (your EFIN will be suspended) and try to entice recipients to open a link or attachment. The IRS urges all tax professionals to be on alert and take security steps to protect their clients and their businesses. Review Publication 4557, Safeguarding Taxpayer Data, for how to be safer.

Notice 2020-17; Payment relief on account of Coronavirus Disease 2019 (COVID-19) emergency. The Treasury Department and IRS are extending the due date for Federal income tax payments due April 15, 2020, to July 15, 2020, for payments due of up to $10 million for corporations and up to $1 million for individuals – regardless of filing status – and other unincorporated entities. Associated interest, additions to tax, and penalties for late payment will also be suspended until July 15, 2020.

Notice 2020-17 will be in IRB 2020-15, dated April 6, 2020.

The IRS established a special webpage on IRS.gov/coronavirus to include all of the available tax-related information. This page will be updated as more information is available.

Treasury News Release: Treasury and IRS Issue Guidance on Deferring Tax Payments Due to COVID-19 Outbreak

QSRA Number: QSRA 2020-01

Issued: January 22, 2020

QSR Topic: Quality Site Requirement #4 – Reference Materials

Reason Issued: Change in policy: Quality Site Requirement (QSR) #4 – Reference Materials

New Policy: QSR #4 is expanded to include the Publication 4299, Privacy, Confidentiality, and Civil Rights – A Public Trust (PDF), as one of the required reference materials that must be available (either in paper or electronic format) at the site for use by volunteers. To heighten awareness of security requirements at VITA/TCE sites, Publication 4299 is now required to be readily available to coordinators and volunteers at the VITA/TCE sites.

References: The Publications 17, 4012 and 4299 are all available for download on IRS.gov or by signing into the TaxSlayer tax preparation software and selecting the option VITA/TCE Publications and User Guides found on the Navigation Bar.

The following VITA Tax Alerts can be accessed with the link below:

VTA-2020-01 Issued January 13, 2020: Tax Law Extenders

VTA-2020-02 Issued January 29, 2020: Form 1099-R Box 7 Distribution Codes • Self-Employed Health Insurance Deduction • Special Rule for Determining Earned Income for Individuals Impacted by Federally Declared Disasters

VTA-2020-03 Issued March 3, 2020: Medicaid waiver payments and refundable credits

Update (11/14/18)

Currently, volunteers may note the following discrepancies when preparing the test return preparation scenarios in the Practice Lab:

o The amount on line 22 of Schedule 1 is incorrect. Amounts from reserved lines 1 -9b are included in the total and shouldn’t be. Therefore, an incorrect amount is being carried over to the left of line 6 on Form 1040. Test answers are not impacted.

o The software is not calculating the Additional Child Tax Credit. The test answers are not impacted.

o The deduction for Qualified Business Income (QBI) is not calculating. Therefore, Form 1040 line 11 (tax), line 15 (total tax), and line 22 (Amount you owe) are overstated. There is a question on the test regarding QBI, but volunteers are not asked to provide the calculation. They should be able to answer the question by reviewing the content on QBI in the training resources.

Keep in mind, the calculation for the Child Tax Credit and Credit for Other Dependents appear on the same line. Volunteers will need to know the tax law to distinguish which credit(s) the taxpayer qualifies to receive, if applicable.

These discrepancies will cease once the software is updated with final forms and instructions.

Fact Sheet Edition: November, 2018

The initial release of the tax year 2018 Practice Lab will not have all the new tax reform changes programmed because the final IRS forms are not yet finalized. We have evaluated the impact to individuals taking the VITA/TCE Certification test. Volunteers should still be able to certify but you should proceed with caution when selecting answers as the Practice Lab may provide tax year 2018 calculations on 2017 forms. TaxSlayer will update the Practice Lab as final forms are approved.

The Practice Lab is tax software that is integrated within Link & Learn Taxes. A link connects students to the 2018 tax preparation software which allows hands-on practice in preparing tax returns.

Combat zone tax benefits now available to Armed Forces members who served in the Sinai Peninsula; IRS accepting retroactive tax refund claims back to 2015

IR-2018-95, April 13, 2018

WASHINGTON — U.S. Armed Forces members who served in the Sinai Peninsula of Egypt may qualify for combat zone tax benefits retroactive to June 2015, according to the Internal Revenue Service.

Under the Tax Cuts and Jobs Act (TCJA) enacted in December 2017, members of the U.S. Army, U.S. Navy, U.S. Marines, U.S. Air Force, and U.S. Coast Guard who performed services in the Sinai Peninsula can now claim combat zone tax benefits. Eligible service members should review Publication 3, Armed Forces’ Tax Guide, available on IRS.gov.

Among other benefits, eligible service members may be able to exclude part or all of their combat pay from their income for federal income tax purposes. Excluding combat pay from a taxpayer’s income can result in lower tax.

How Armed Services members can claim a refund

Service members who previously paid tax on this income may be due a refund. They may file an amended tax return, Form 1040X, if they already filed a tax return for tax years 2015, 2016 and 2017.

Combat pay received on or after Jan. 1, 2018, will be correctly reported on any W-2 forms issued to any service member who serves in the Sinai Peninsula. Service members who served in the Sinai Peninsula in 2015, 2016, or 2017 can provide documentation of their service to their finance officer and ask for a Form W-2c, Corrected Wage and Tax Statement.

However, an eligible service member who is unable to secure a corrected Form W-2c may still claim the combat pay exclusion by attaching to their Form 1040X copies of official documents showing they served or worked in the Sinai Peninsula. These documents should indicate the area, theater or military operation and the approximate entry date. Acceptable documents include military orders, letters of authorization (civilians), hospital discharge papers, discharge from active duty, official letterhead memorandum from a military department or civilian employer, or a request and authorization for temporary duty travel of Department of Defense personnel (civilians and military).

Amended returns can only be filed on paper (electronic filing is not available) and can take up to 16 weeks to process. Within about three weeks after mailing an amended return, taxpayers can track the status online using Where’s My Amended Return?

For more information about requesting a refund based on service in the Sinai Peninsula, see the Form 1040X instructions, available on IRS.gov.

For the week ending 4/08/2018, we were just shy of the 3.0M cumulative mark, but we will pass it for sure next week! We prepared 305,634 returns, with a cumulative total of 2,958,004.

Many of our partners have extended their hours, added additional days, and planned special events to help this valiant effort of touching more lives!

Hats off to everyone!

Stay the Course!

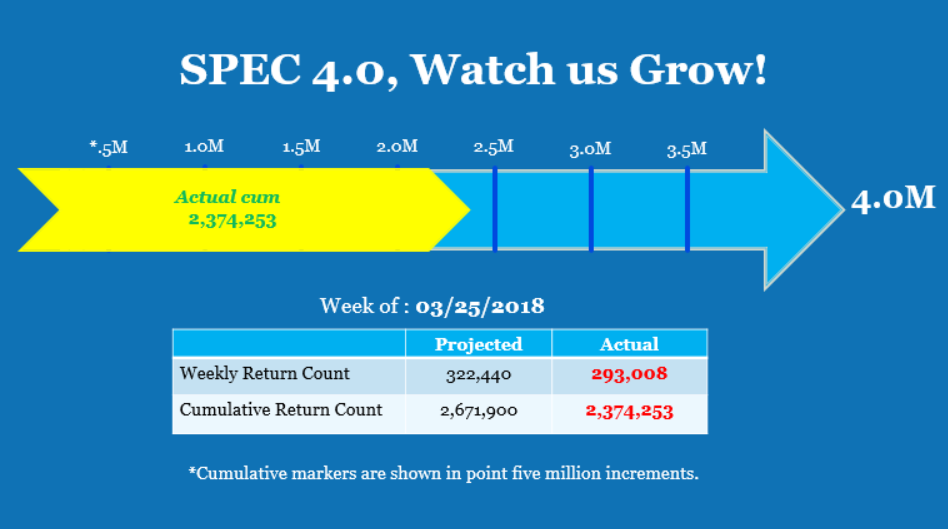

With just a little more than two weeks before April 17th, we are steadily moving towards our 4.0 goal, as reflected in our numbers for the week ending 3/25/2018. We will stay the course until the job is done!

Kudos to everyone for helping prepare 293,008 returns! Yes, we are a little short of our weekly projection, but compared to last year, this represents a 2.3% increase. As you can see below, we are quickly approaching the 2.5M cumulative mark. Hats off for achieving a 0.1% increase above last year!

Even with the continued weather challenges in some areas, we continue to see increases in our FSA and prior year return preparation numbers, 5.9% and 53.3% respectively. We’ve also seen a 1.9% increase in our state tax return preparation. Keep it up!

Halfway There!

Keep up the good work!

First, we want to thank each of you for your dedication and commitment to make this a banner year for return production. SPEC’s goal is not only to reach 4 million returns for Filing Season 2018, but also serve more taxpayers and touch more lives by offering as many free tax preparation options as possible. We are confident and poised to accomplish great things this filing season with your assistance.

To help track our progress, we have developed weekly projections to determine where we should be in relation to our 4.0 goal. Each week this message will be updated with our progress and promote SPEC’s theme: SPEC 4.0, Watch us Grow!

For the week ending 3/4/2018, 356,317 returns were projected to be completed. We reached an actual count of 313,542 and are almost at the 1.5 million mark. Our cumulative return count is 1,468,961.

While the actual count is below the SPEC projection, there is still time to narrow the gap!

If you have any ideas on ways to help this initiative, we would love to hear from you! Some of you may consider extended hours or days. Every little bit helps!

Thanks for your engagement and all you are doing to provide free tax assistance to the taxpayers in your community!

SPEC Headquarters