2/22/23 – This is now resolved.

Update 2/20/23: The deployment on Friday, February 17th corrected the calculation issue related to Line 5 of the IL-1040. However, the display in the PDF is still incorrect and does not reflect the accurate refund/amount owed on Line 37 or 40. The Return Summary (example below) is correct and that is the value the TP can expect to owe or receive as a refund. NOTE: The electronic submission is correct and the amount reflected in the Return Summary is what is sent with the electronic submission. It is ok to resume electronically filing impacted IL returns.

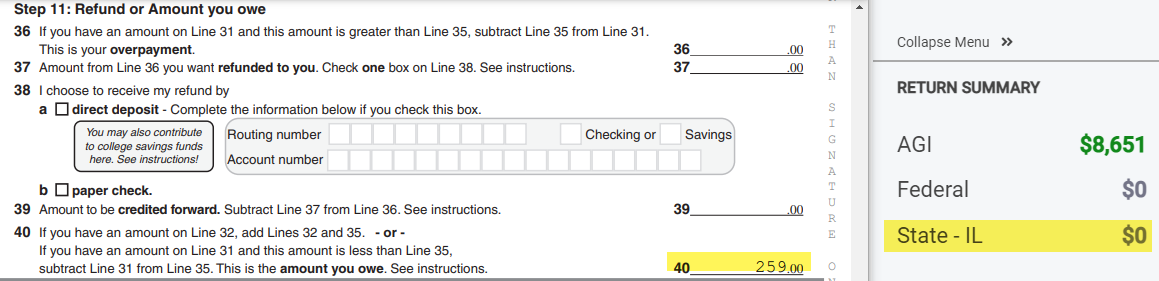

So, looking at the screenshot below, the PDF (IL return) incorrectly shows the TP owes $259 (Line 40 of IL-1040). Their Return Summary correctly reflects the TP does not have a tax liability and will not receive a refund from IL.

Update 2/17/23: The fix was rolled back due to an unforeseen issue. We are currently working to resolve this issue.

The fix for this should be deployed Friday morning, February 17th.

We are aware of an issue that began this morning (2/15/23) where entries in the subtractions from income menu within the Illinois application are not carrying to the return. We have a high priority ticket in with our development team.